EU VAT changes valid from January 1st 2020

Starting from 1st January 2020, new rules intended to harmonise and simplify VAT rules of certain intra-Community operations are coming into force. These rules are commonly being referred to as “Quick Fixes” and may concern your company.

We are drawing your attention to the fact that these measures are mandatory and require perfect coordination with other parties in your operations in particular your suppliers, your clients and your carriers.

Quick Fixes - EU VAT 2020

You will find below an overview of these new measures. This document is intended to inform you of the major changes these measures bring. Our team is of course at your disposal to respond to all your questions in regards to this topic.

New conditions for VAT exemption

Ensuring exemption of VAT on Intracommunity supplies is subject to three new conditions:

- Obtaining proof of the purchaser’s VAT number, issued by the National Tax Administration of a Member State of the European Union different to the Member State from which the goods will be shipped, before the operation takes place. Your company will have to check this VAT number for each intracommunity supplies of goods and must keep evidence that the number has been correctly validated (for example using the VIES VAT number validation system),

- Having previously filed an Intrastat return on dispatch,

- Being in possession of additional evidence that goods have indeed left the country of departure. In addition to signed and stamped CMR documents, other documents must be kept by the seller in order to justify VAT exemption. Companies are therefore asked to supply two pieces of evidence showing that the delivery took place. This evidence must be issued by two different parties. For example, an invoice issued by the carrier, a payment document, or any other proof that can be analysed by the Tax Administration can be used.

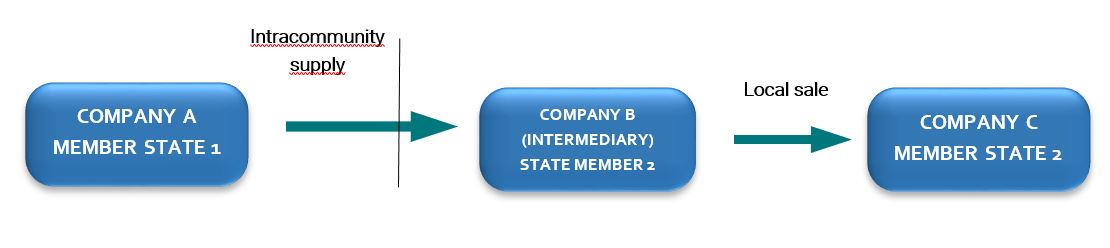

Chain transactions and intracommunity deliveries

Chain transactions are defined as successive sales of goods between several taxable entities and where one single transport operation occurs from the Member State of the seller to that of the final recipient. The main question asked before the "quick fixes 2020" by operators was knowing whether it was the supplier, the intermediary parties, or the client who could benefit from VAT exemption.

Starting from 1st January 2020, a common rule is implemented according to which VAT exempted deliveries shall be those carried out by the initial supplier to an operator defined as an intermediary, who in this case will be in charge of transporting the goods. As a general rule, intermediary operators are considered to be the operator in charge of ensuring the transport of goods.

However, if this intermediary operator gives the supplier its VAT number, which has been issued by the Member State from which the goods will be shipped:

- The first sale from the supplier to the intermediary operator will be qualified as a domestic sale in the country of departure of the goods,

- The second sale, taking place between the first intermediary operator and the next intermediary will be considered VAT exempt, as it is this operation that will be qualified as an intra-Community delivery.

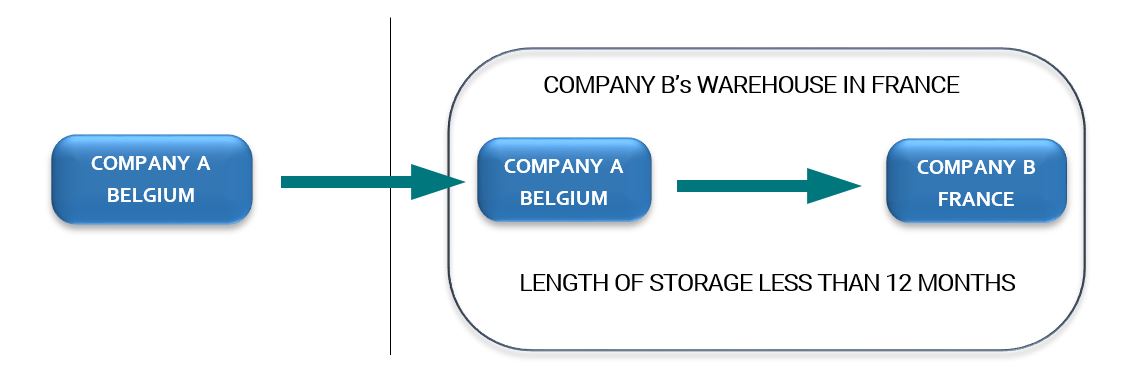

Using a call-off stock in another Member State

A call-off stock is defined as a movement of goods within the premises of a client, who takes goods from the stock as and when they are needed.

In principal, the use of a call-off stock in another Member state is done in two stages:

- A transfer of goods from a stock based in one Member State of the European Union to a stock located in another Member State,

- An internal sale taking place in the Member State where the call-off stock is situated (VAT registration is necessary in this country for the seller).

Starting from 1st January 2020, transfer of goods to call-off stocks are simplified. Suppliers no longer have the obligation to register for VAT in the country where the goods are being stored, so long as:

- The supplier does not own a permanent establishment in the country of destination,

- The party receiving the goods is registered for VAT in the country of destination,

- The goods must be sold to the recipient in a delay of 12 months following their arrival in the call-off stock,

- The transfer is correctly recorded in a dedicated register.

According to the simplifcation and if the lenght of storage is less than 12 months (as in the example above) :

- Company A submit an Intrastat return on dispatch to the company B at the time of the shipment of the goods,

- Company A reports an Intracommunity delivery in a Belgian VAT return at the time of the sale of the goods to the company B,

- Company B reports an Intracommunity acquisition in a French VAT return and in a French Intrastat return on arrival if the French yearly threshold of 460.000€ for Intracommunty acquisitions in reached.

The application of this measure naturally requires the agreement of your client as they will become liable for new obligations regarding VAT and Intrastat returns.